This page is about balancing your investments each year. It’s a technique that I’ve seen mentioned and heard of friends using, but I’ve never found maths to justify it. So here’s some maths and some interesting conclusions.

The underlying idea is to cash in a year of high growth in one investment and rebalance it into an investment that has underperformed this year and (you hope) will bounce back. It’s supposed to take the tinkering human out of the equation (holding investments too long, selling low and buying high), and instead have a process that can be followed automatically. It can be applied across a portfolio: e.g. every June you rebalance your investments to be 40% UK Income, 20% North America, 20% Corporate bonds, 20% Gilts.

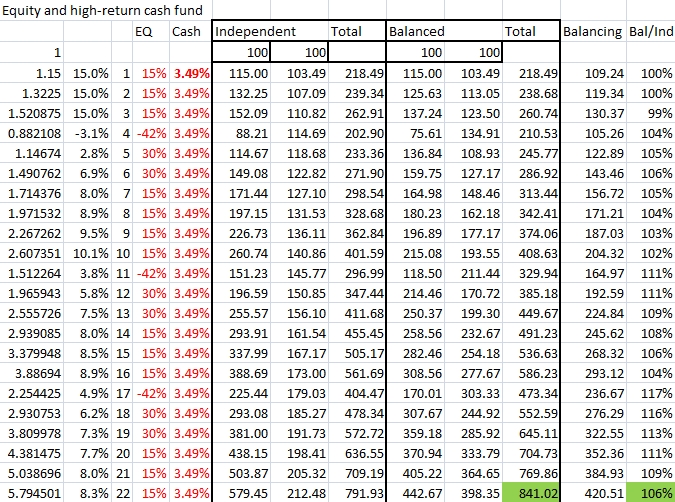

What’s in the tables

In this analysis there’s “Equity” which achieves 8.3% annual return, “Flip” which rises when equity falls though not so volatile, “Cash” with a constant and generous 3.49%, “Corporate Bond” which moves in phase with equities but is much less volatile, and “Low-volatility equity” which achieves 8.4% but with less volatility (and is of course totally unrealistic). For three of the scenarios we have all-equities but their falls and recoveries are out of phase by a defined number of years.

The columns to the left show the annual performance of the two investments over 22 years. Then you see the performance if we leave the investments independent and don’t balance, starting with both valued at 100. Then the year end values if we balanced at the end of the previous year (and you also see that balanced figure). Finally there’s the ratio of the balanced total divided by the independent total: over 100% in year 22 means that balancing has helped.

Historical data and loss aversion

The rather fascinating website “PortfolioCharts” uses historical data to analyse portfolios with significant proportions of bonds, gold, cash, equities, etc.. It assumes rebalancing annually. I think(!) the various equity groups (small cap, Europe, emerging markets, etc.) are modelled based on historical data, so whether they are rising and falling in phase with each other or out of phase depends on actual historical data.

I could return to it again and again, but it has some key criteria that I don’t totally believe suit me. (1) For younger pension investors with many years to build a sum, volatility is not an issue so 100% equities seems the best bet for growth. That’s not me any more but it’s worth bearing in mind, especially if I withdraw only a very low percentage in some years, and it explains why I have been happy with 100% equities while I was building up my pension pot. (2) If I accept that I will adjust my pension spend annually up or down to reflect market performance, I will not run out of money. If I fully accept the volatility then in the long term I am most likely to get the best total return from 100% equities. (3) About half my “minimum” pension budget would be covered by state pension and DB pension, so in a bad year I am withdrawing very little from the pension pot. (4) My pension planning includes large one-off sums for changing my car every 4 or 5 years. These sums can be deferred if necessary in the model, which partly offsets bad years. (5) The various analyses in PortfolioCharts assess multiple spans of years and focus on the worst span, combined with various choices of rules for adjusting pension income each year, as a way to offer a good chance of not reducing the annual pension. This emphasis on loss-aversion is not something with which I feel very comfortable.

Those rules for adjusting pension income are interesting. One option is to increase my pension in line with inflation unless the pot moves beyond a certain point. This allows for cyclic market variation without having a similarly cyclic income. I find the rules the most interesting part: I can leave the portfolio with 100% equities and apply different rules to see which are likely to cause the pot to be exhausted as well as seeing what minimum and maximum pension could be taken from a pot.

Conclusions

First remember that I value growth. I do not have a problem with volatility. If you have a problem with volatility then you might make some different conclusions.

Second remember that hindsight is a wonderful thing. In these examples all equities return 8.3%, cash returns 3.49%, etc.. Should you invest in Emerging Markets Growth in the hope of holding an investment that performs as well as North America but with different phasing? Or would you be better with South East Asia? In real life, the best performance could come from 100% investing in the one thing that outperforms everything else, but who knows which that is?

I see that in pretty much every case, it is better to rebalance than to leave funds alone.

I see that the best final total comes from investing in high-growth investments. Blending equity-bond or blending equity-cash might reduce volatility but it doesn’t reach the heights that blending equity-equity achieves (assuming equities perform best!!).

I see that balancing equities that are slightly out of phase gives best results (a crash in one lines up with a recovery from a crash in the other).

I see that more volatile investments balanced with each other do better than less volatile investments balanced with each other. This leads to a rather horrible conclusion: artificial instruments that amplify the performance of an equity market (deeper losses, greater rises) balanced with an out-of-phase amplified investment perform best. Whatever you think of the suitability of such investments, a follow-on is that people stand to benefit from stock market volatility and therefore some will work to achieve it.

So overall, don’t be surprised if I continue to chase high-growth equities. I rebalance rather thoughtfully – trying to anticipate the imminent growth area and being overweight there – and I know I hang onto one or two great performing funds or shares (Rio Tinto), when probably I shouldn’t. Perhaps I should just balance automatically.

![]()